Industrial real estate shifts focus in U.S. and Canada

Precision, not square footage, will define industrial real estate

SOURCE: RSM CANADA

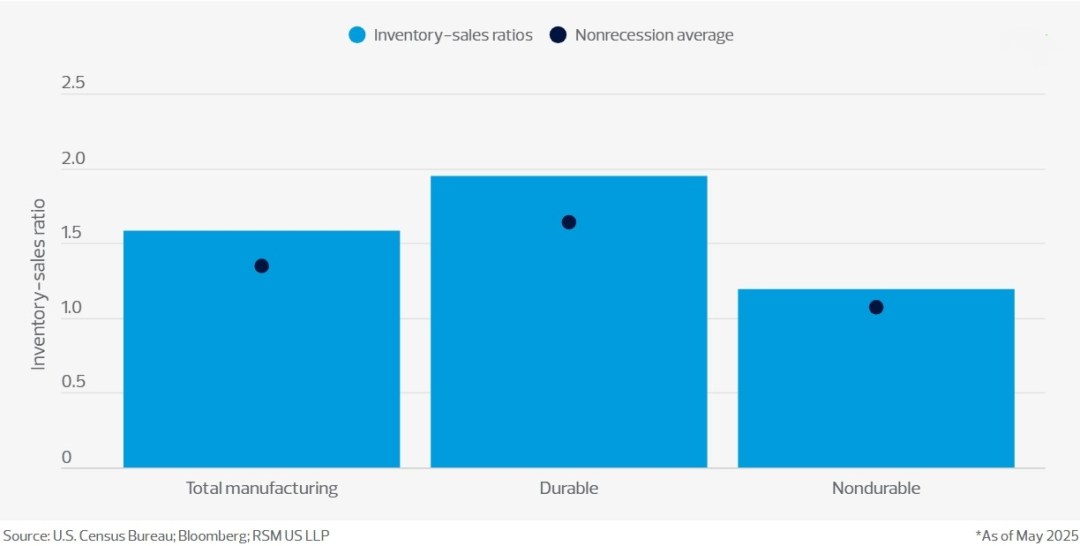

Industrial real estate is undergoing a significant shift driven by cooling tenant demand, tariff pressures and evolving supply chain strategies. The focus is moving from sheer square footage to precision in functionality and resilience, reflecting broader economic and technological changes. U.S. firms pulled economic activity forward into the first half of 2025, restraining inflation growth. However, inventory overhangs remain well above nonrecessionary averages, suggesting businesses are holding excess supply. Stockpiles of durable goods—particularly machinery, metals and automobiles—remain elevated, pointing to an expected manufacturing slowdown as weak housing and auto demand collide with rising tariff risk.

As inventories are gradually worked down, inflationary pressures are likely to build in the second half of the year. With limited upside from tariffs and retailer caution, restocking and import activity should remain subdued.

Manufacturing inventory-sales ratios*

Trucking is already feeling the strain of the uncertainty in its restocking decisions and slow imports. Loaded truck crossings into the U.S. fell 13% from Canada and 6% from Mexico in April 2025, per the U.S. Department of Transportation. Canada is being hit harder than Mexico because it supplies a far greater share of U.S. steel and aluminum imports—products directly targeted by tariffs—magnifying the trade shock north of the U.S. border. Small and midsize haulers are especially vulnerable to this shock.

Refinancing risk and shifting capital strategies

Commercial real estate loan quality is deteriorating just as the industry confronts a historic refinancing wall. Past-due and nonaccrual rates for CRE are at their highest since 2014, with large banks reporting a 4.65% rate on non-owner-occupied loans—nearly eight times above prepandemic norms, per the U.S. Federal Deposit Insurance Corp. At the same time, $1.8 trillion in loans are maturing by 2026, according to NAIOP, the Commercial Real Estate Development Association. Much of it is predicated on vintage 2020 debt priced at exceptionally low interest rates. With returns under pressure and traditional refinancing routes strained, firms are turning to asset sales, restructurings and, increasingly, private equity and credit to fill the gap.

Vacancy, construction slowdown and market recalibration

The third-party logistics boom of 2021–22, fueled by e-commerce and strong imports, collapsed by late 2023. Dozens of logistics firms went under, and excess warehouse space flooded the market. National industrial vacancy reached a decade high of 7.5% in Q2 2025 as industrial deliveries continue to outpace absorption, meaning new industrial buildings are completed faster than tenants lease space.

Industrial deliveries continue to outpace absorption, increasing vacancy

More space is being vacated than leased, resulting in negative net absorption. This can be attributed to big-box retailer bankruptcies and logistics companies like UPS and FedEx reducing space due to normalized package demand, downsizing and increased automation. This has led to sellers offering large vacant warehouses at steep discounts, softening rents with only a 0.8% increase year over year in early 2025, according to the commercial real estate information company CoStar.

Rising tariffs on steel, aluminum and other core construction materials are raising local input costs, while tight labor markets and macroeconomic uncertainty are freezing new starts. With just 52.6 million starts in Q2 2025, construction activity hit its slowest pace since Q1 2015—well below the quarterly average of 87.6 million, per CoStar. The market is shifting focus from new builds to targeted redevelopments and adaptive reuse. Global companies are consolidating U.S. operations to reduce cross-border exposure, increasing sublease availability in Canada as these companies vacate or downsize space amid tapering demand. Some recently completed buildings in Canada are back on the market.

Canada sublease space on the rise

Capital is flowing to execution, not expansion

Investment capital is pivoting from scale to control, with owner/user transactions exceeding $1 billion in late 2024 and early 2025, accounting for 34% of Q1 2025 volume, per CoStar. Private capital dominated deals under $25 million, while institutional buyers captured 45% of Q1 volume over $50 million. Industrial sales rose 25% year over year, per CoStar, with investors focusing on operational upside, shorter leases and embedded rent growth rather than just square footage. Large, empty warehouses traded at wider discounts, while small-bay industrial spaces with sub-4% vacancy and 50% leasing growth, especially in the Southern and Midwestern United States, attracted private capital due to limited new supply and flexible layouts suited to an agile economy.

The Outlook: From build-to-core to build-to-function

The new industrial real estate playbook is about resilience, functionality and execution. Tenants want less friction and more control while investors want less exposure and more precision.

Trends such as automation, adaptive reuse, digital infrastructure and decentralized logistics mark 2025 as an inflection point. Ultimately, industrial real estate value will be defined not by the amount of space controlled but by how effectively that space enables tenant operations, supports supply chain efficiency and accommodates capital investment.